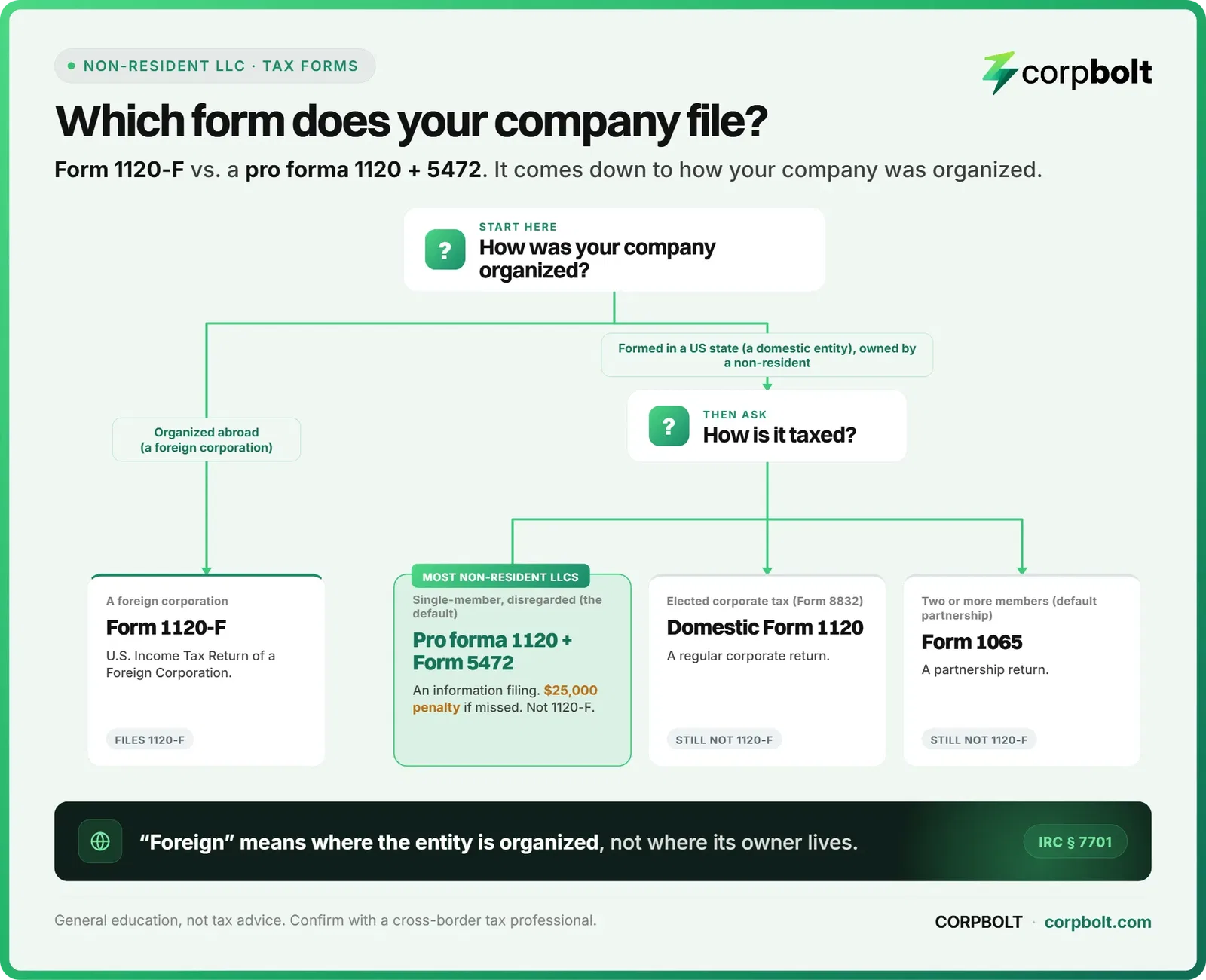

If you are a non-resident who owns a US-formed single-member LLC, such as a Wyoming LLC, Form 1120-F is almost certainly not your form. Form 1120-F is a foreign corporation's US income tax return, and a US-formed LLC is a domestic entity no matter where its owner lives. Your default federal filing is usually a pro forma Form 1120 with Form 5472 attached, which is an information return rather than a tax bill. Because tax turns on your exact facts, confirm your own filing with a qualified cross-border tax professional.

Its official title is the "U.S. Income Tax Return of a Foreign Corporation," and every filing trigger assumes a corporation organized outside the United States.

In tax law "foreign" means organized outside the US. A company formed in Wyoming is domestic even when every owner is a non-resident.

A foreign-owned US LLC that is disregarded generally files a pro forma Form 1120 with Form 5472, an information filing with a $25,000 penalty for missing it.

Form 1120-F is one of the most misread forms for non-resident founders, and the confusion is understandable: you are a foreign person, so it feels natural to assume your company files the "foreign corporation" return. In most cases it does not. The word that trips people up is "foreign," and it does not mean what it seems to here. This guide, written for a non-resident who owns a Wyoming LLC, explains what Form 1120-F actually is, who really files it, and what a foreign-owned US LLC files instead. It is general information for education, not tax or legal advice, and because the right answer depends on your specific facts, treat a qualified cross-border tax professional as the final word.

Foreign corporation vs. your US-formed LLC: the distinction that settles it

Almost the entire Form 1120-F question comes down to one line in the tax code, and it is not about you. It is about where your company was organized. Under the definitions in section 7701 of the Internal Revenue Code, an entity is "domestic" if it is created or organized in the United States or under the law of the United States or any state. An entity is "foreign" if it is not domestic. The IRS says the same thing in plainer words for corporations: a foreign corporation is one created or organized outside the United States, and a domestic corporation is not a foreign corporation.

Read that against your own company. A Wyoming LLC is formed under Wyoming state law, so it is a domestic US entity. Nothing about that changes because its owner lives in London, Dubai, or anywhere else. The residency or citizenship of the owner is a separate question from where the entity itself is organized. It is the entity's place of organization, not the owner's passport, that decides whether a return is a "foreign corporation" return. That is the whole reason a foreign-owned Wyoming LLC does not, on its own, land on Form 1120-F.

What Form 1120-F actually is, and who really files it

Form 1120-F is officially the "U.S. Income Tax Return of a Foreign Corporation." A foreign corporation uses it to report its US income, gains, deductions, and credits, and to figure the US income tax it owes. Every category of filer in the instructions starts from that same premise, a corporation organized abroad, and then asks what US connection it has. Broadly, a foreign corporation generally files Form 1120-F if it was engaged in a US trade or business during the year, or if it had US-source income whose tax was not fully satisfied by withholding at the source. Narrower cases also apply, such as claiming a refund, claiming the benefit of a tax treaty, or acting as a qualified derivatives dealer.

How a foreign corporation is taxed on that return is worth understanding, if only to see that it describes machinery your pass-through LLC does not run. Income that is effectively connected with a US trade or business is generally taxed on a net basis at the regular corporate income tax rate, a flat 21 percent for tax years beginning after 2017, meaning related deductions are allowed. Other US-source income that is not effectively connected, often called FDAP income, is generally taxed on a gross basis at a flat 30 percent rate, or a lower rate under a treaty, with no deductions. On top of the regular tax, a foreign corporation with a US branch can face an additional branch profits tax.

As for timing, a foreign corporation with a US office generally files by the fifteenth day of the fourth month after its year end. One without a US office files by the fifteenth day of the sixth month, with an extension available on Form 7004. Confirm the current rules and dates in the IRS instructions, because they can change.

The return also carries machinery for the harder cases a genuine foreign corporation faces. A company that is unsure whether its US activity produces effectively connected income can file a protective Form 1120-F, which safeguards its right to claim deductions and credits. That protection matters because a foreign corporation that files no return loses those deductions and credits against effectively connected income and can be taxed on its gross US income instead. Tax treaties add another layer. A treaty can decide whether the company has a US permanent establishment, and so whether it counts as engaged in a US trade or business. Even income a treaty exempts must still be reported on Form 1120-F, with the treaty position disclosed on an attached Form 8833. Treaty relief can remove the tax without removing the return. The form then separates income that is effectively connected from income that is not, and carries schedules that allocate the deductions. None of this apparatus is triggered by simply owning a US LLC from abroad.

What a foreign-owned US LLC files instead

Here is the return that usually does apply. By default, a single-member LLC is a disregarded entity, which the IRS treats as not separate from its owner for federal income tax, unless the LLC elects to be treated as a corporation. A US LLC that is disregarded and owned by a foreign person sits under a specific reporting rule. As a result of regulations under section 6038A, a foreign-owned US disregarded entity is required to file a pro forma Form 1120 with a Form 5472 attached. The point that catches people out is the nature of this filing: Form 5472 is an information return that reports transactions between the LLC and its foreign owner, not a calculation of income tax the LLC owes.

The pro forma Form 1120 here is deliberately thin. The IRS instructions ask you to complete only the name and address of the entity plus a couple of identifying items on the first page, and to write "Foreign-owned U.S. DE" across the top. The substance is carried by the attached Form 5472. This package cannot be e-filed, so it is sent to the IRS by mail or fax. To file it you will need an EIN for the LLC, which is a separate step covered in what an EIN is. The comparison below lines up the two returns side by side.

Form 1120-F | Pro forma Form 1120 + Form 5472 (your LLC) | |

|---|---|---|

Who files it | A foreign corporation, one organized under the laws of a country outside the United States | A US-formed LLC, such as a Wyoming LLC, owned by a non-resident and treated as disregarded |

What it is | The foreign corporation's US income tax return | An information return reporting transactions between the LLC and its foreign owner |

Does it figure a US tax? | Yes, it computes the corporation's US tax on its US-connected income | No, by itself it reports information and does not calculate a tax the LLC owes |

How you file it | By its own 4th- or 6th-month deadline; extendable on Form 7004 | Mailed or faxed to the IRS; it cannot be e-filed |

Penalty for not filing | Late-filing and late-payment penalties; filing very late can forfeit deductions and credits | A $25,000 penalty for a missing or incomplete Form 5472 |

The one time a US LLC touches a corporate return, and it is still not 1120-F

There is a narrow case where a US LLC does file a corporate return, and it helps to name it precisely so it does not muddy the rule. An LLC can file Form 8832 to elect to be taxed as a corporation instead of as a disregarded entity or partnership. If it makes that election, it then files Form 1120, the standard US corporation income tax return. Notice what has and has not changed. The LLC is still organized under US state law, so it is still a domestic entity, and a domestic entity that is taxed as a corporation files the domestic Form 1120, never Form 1120-F. A 25 percent foreign-owned domestic corporation also has its own Form 5472 reporting. This is described here only as a factual carve-out, not as a move to make; whether any tax election makes sense is exactly the kind of decision to run past a professional.

One more boundary is worth drawing so the disregarded-entity path is not over-applied. The pro forma 1120 plus 5472 route is the default for a single-member LLC. A US LLC with more than one owner defaults instead to a partnership, which files Form 1065, a different track again, and still not Form 1120-F. And whether any of your activity rises to a US trade or business or produces US-source income is a fact-specific question in its own right. Income that is connected to the US can also create a separate US return for you as the owner, such as a Form 1040-NR, which is again a matter for your tax professional. The through-line across all of these is simple: a US-formed LLC is a domestic entity, and domestic entities do not file the foreign-corporation return.

The bottom line for a foreign-owned Wyoming LLC

If you own a US-formed single-member LLC as a non-resident, the most likely reality is that Form 1120-F is not your form. Your annual federal filing is instead a pro forma Form 1120 with Form 5472 attached, an information return carrying that $25,000 penalty if it is missed. Form 1120-F belongs to corporations organized outside the United States, which your Wyoming LLC is not. Because the details depend on your ownership, your activity, and any elections you have made, use this as orientation rather than a filing instruction, and confirm what your company actually files with a qualified cross-border tax professional. CORPBOLT is a formation service, not a law or accounting firm, as explained in whether CORPBOLT provides legal or tax advice.

Frequently asked questions

Does my foreign-owned US LLC file Form 1120-F?

Usually not. Form 1120-F is a foreign corporation's US income tax return, and a US-formed LLC is a domestic entity regardless of where its owner lives. A foreign-owned single-member LLC that is disregarded generally files a pro forma Form 1120 with Form 5472 instead. Confirm your own case with a cross-border tax professional.

What is the difference between Form 1120-F and Form 5472?

Form 1120-F is a foreign corporation's actual income tax return that figures US tax owed. Form 5472 is an information return that a foreign-owned US LLC files, attached to a pro forma Form 1120, to report transactions with its foreign owner. One computes a tax; the other reports information.

Why is my Wyoming LLC "domestic" if I live abroad?

Because tax law defines "domestic" and "foreign" by where the entity is organized, not by the owner's residence. Under section 7701, an entity organized under US or state law is domestic. A Wyoming LLC is formed under Wyoming law, so it is domestic even when its owner is a non-resident.

When would a US LLC ever file a corporate return?

If it files Form 8832 to elect corporate tax treatment, it then files Form 1120, the domestic US corporation return. It remains a domestic entity, so it still does not file Form 1120-F. That is an election to weigh with a professional, not a default.

What happens if I file the wrong form or miss Form 5472?

The IRS sets a $25,000 penalty for failing to file a required Form 5472. Filing Form 1120-F when it does not apply, or overlooking the pro forma Form 1120 and 5472 that do, can both cause problems. The safe step is to confirm your filing obligations with a qualified cross-border tax professional.

Who actually files Form 1120-F?

A foreign corporation, meaning one organized under the laws of a country outside the United States, generally files Form 1120-F if it was engaged in a US trade or business, or had US-source income not fully covered by withholding. Narrower cases include claiming a refund or a treaty benefit. A US-formed LLC does not fit that description.

Can a foreign corporation file Form 1120-F protectively?

Yes. A foreign corporation that is unsure whether its US activity creates a tax obligation can file a protective Form 1120-F, which preserves its right to claim deductions and credits. Without a filed return, a foreign corporation loses those deductions and credits against effectively connected income and can be taxed on its gross US income. This is a foreign-corporation question, though. A foreign-owned US LLC files Form 5472 with a pro forma Form 1120, not a protective 1120-F.

How this article was prepared

CORPBOLT prepared this guide for non-US founders who own a Wyoming LLC. The official title of Form 1120-F and its "Who Must File" categories, the effectively connected income and FDAP tax treatment, the branch profits tax, and the filing deadlines are drawn from the IRS About page and Instructions for Form 1120-F. The rule that a foreign-owned US disregarded entity files a pro forma Form 1120 with Form 5472, the pared-down pro forma contents, the mail-or-fax filing, and the $25,000 penalty are from the IRS Instructions for Form 5472. The disregarded-entity default and the Form 8832 corporate election are from the IRS single-member LLC guidance. The definition that separates a "domestic" from a "foreign" entity, and the point that a foreign corporation is one organized outside the United States, are from section 7701 of the Internal Revenue Code and the IRS foreign-corporation filing-responsibilities page. The protective-return rule, the treaty and permanent-establishment points, and the Form 8833 disclosure are from the Instructions for Form 1120-F and the IRS About Form 8833 page, all linked below. Tax outcomes depend on your specific facts, so this is general education, not tax or legal advice, and CORPBOLT is a formation service rather than a law or accounting firm. Confirm your own filing with a qualified cross-border tax professional. Last reviewed July 2026.

Build your LLC on a clean base with CORPBOLT: getting your federal filings right starts with a properly formed and maintained entity. CORPBOLT forms and maintains Wyoming LLCs for non-residents from $349/year (Foundation), including the registered agent and annual upkeep. The EIN you will need to file Form 5472 is included from $599/year (Launch) or available as a $199 add-on. The pro forma Form 1120 and Form 5472 themselves are best handled with a qualified cross-border tax professional. Form your Wyoming LLC →

Official references

IRS: About Form 1120-F, U.S. Income Tax Return of a Foreign Corporation

IRS: Instructions for Form 5472 (pro forma 1120 for a foreign-owned U.S. DE)

IRS: Foreign corporation Form 1120-F filing responsibilities

IRS: About Form 8833, Treaty-Based Return Position Disclosure

Important: This article is for general information only and is not legal or tax advice. Requirements can vary by state, provider, and individual circumstances, so consider speaking with a qualified legal or tax professional before making filing, tax, banking, or payment decisions. Eligibility and approval decisions are made by each bank, fintech, and payment processor.