You must file Form 5472 if your US LLC is at least 25% foreign owned and had a reportable transaction with a related party during the tax year. A wholly foreign-owned single-member LLC counts, because the IRS treats it as a corporation for this one rule. It files a pro forma Form 1120 with Form 5472 attached, and a missed filing carries a $25,000 penalty.

You file because your foreign-owned LLC had a reportable dealing with its owner or another related party, such as the money you put in to fund it. This is a reporting duty, not a tax bill.

For section 6038A, the IRS treats a wholly foreign-owned disregarded entity as a corporation. So your one-owner LLC files Form 5472 attached to a near-empty pro forma Form 1120.

It is due the 15th day of the 4th month after the tax year ends, about April 15 for calendar-year filers, or later with a Form 7004 extension. Filing late or not at all triggers a $25,000 penalty.

Who must file Form 5472?

Form 5472 is the IRS Information Return of a 25% Foreign-Owned U.S. Corporation or a foreign corporation engaged in a US trade or business. It reports dealings between that entity and its related parties under section 6038A.

Form 5472 is filed by what the IRS calls a reporting corporation. Two kinds of entity fit that label. The first is a 25% foreign-owned US corporation, and the instructions expressly include a foreign-owned US disregarded entity in that group. The second is a foreign corporation engaged in a trade or business inside the United States.

For most non-resident founders, only the first branch matters. If your US LLC has at least one 25% foreign owner and had a reportable transaction with a related party during the year, it is a reporting corporation and it files Form 5472. The rest of this guide unpacks each piece of that test.

Does a foreign-owned single-member LLC really have to file?

Yes, and this is the part that surprises people. By default a single-member LLC is a disregarded entity for federal tax, meaning the IRS looks through it to its owner. That default has not changed for income tax. It changed only for information reporting.

The section 6038A regulations changed that for tax years beginning after December 31, 2016. Under those rules, a domestic entity wholly owned by one foreign person is treated as separate from its owner. For the limited purposes of this reporting, it is classified as a corporation. In plain terms, your one-owner LLC is still disregarded for tax, yet it must report like a corporation on Form 5472.

Because it has no income tax return of its own, it files a pro forma Form 1120 as a cover and attaches Form 5472 to it. Pro forma means for the sake of form, so you complete only the entity name, address, and identifying details on the 1120. Our guide to the pro forma Form 1120 and Form 5472 walks through which parts to complete and what transaction details to gather, step by step.

What makes someone a 25% foreign owner?

The 25% test looks at ownership, not at where you live day to day. A company is 25% foreign owned if it has at least one direct or indirect 25% foreign shareholder at any point during the tax year. A single foreign owner of a one-member LLC clearly meets that bar.

A 25% foreign shareholder is a foreign person who owns at least 25% of the company by either of two measures, a test set in Internal Revenue Code section 6038A(c). The first is the total voting power of all classes of ownership. The second is the total value of all classes. Meeting either one is enough, and a foreign person includes a nonresident individual or a foreign company.

What is a reportable transaction that triggers the filing?

Being 25% foreign owned is not enough on its own. The filing is triggered only when the reporting corporation has a reportable transaction with a related party during the year. A related party includes the foreign owner and other people or companies connected to them.

A reportable transaction is any of the dealings the form lists in its Part IV, where money was the only consideration. Common examples include:

Sales or purchases of goods, and payments of rent, royalties, or interest.

Loans between the LLC and its owner or another related party.

Amounts tied to forming, dissolving, acquiring, or disposing of the entity.

Contributions into the LLC and distributions back out to the owner.

That last point is why so many single-member LLCs have a filing. When you fund your own LLC, that capital contribution is itself a reportable transaction between you and a related party. Paying the LLC costs from your personal account can count too.

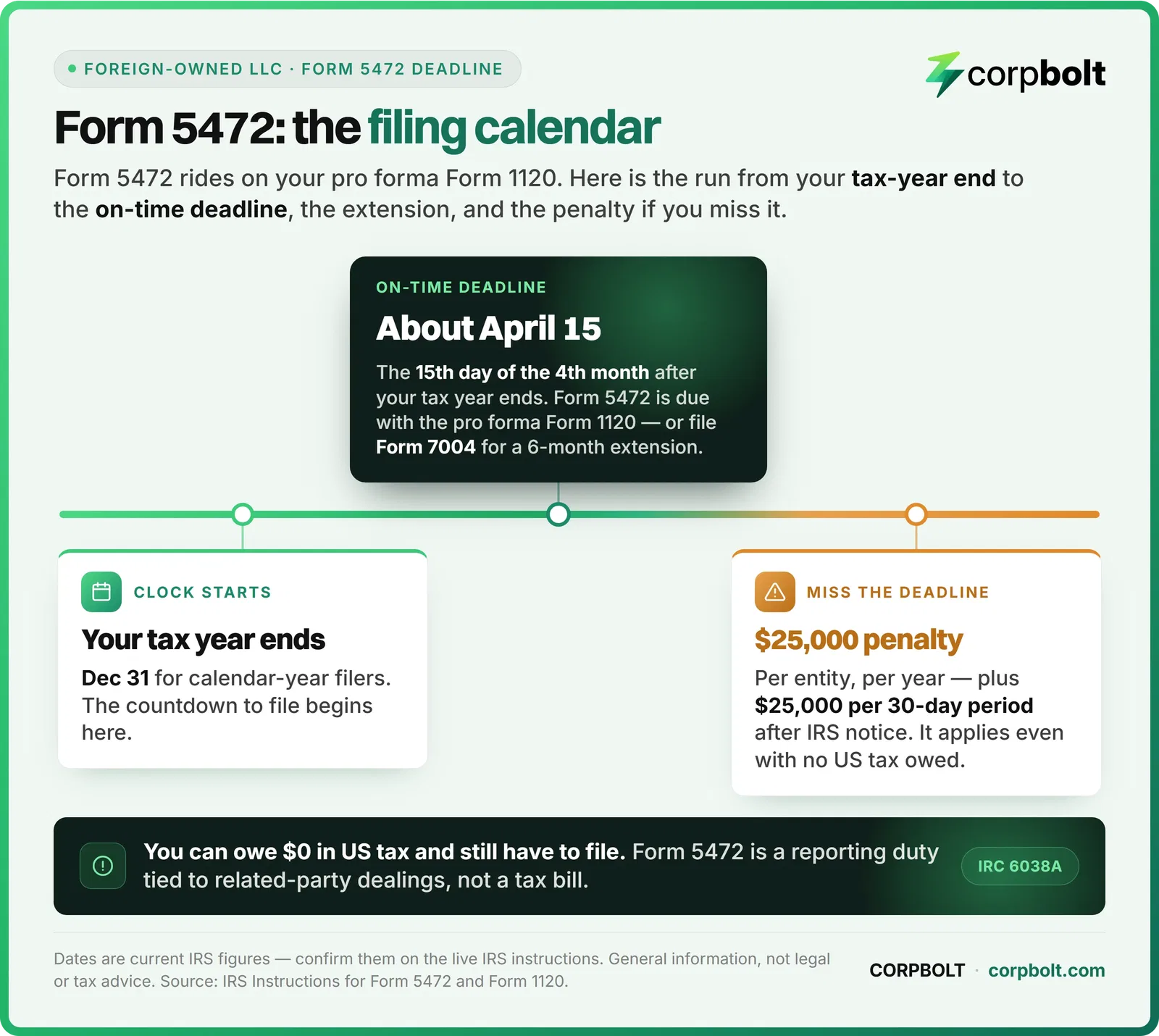

When is Form 5472 due, and can you extend it?

Form 5472 does not have a separate deadline. It is due with the income tax return it rides on, by that return due date including extensions. For a foreign-owned LLC pro forma Form 1120, that is the 15th day of the 4th month after the tax year ends.

For a calendar-year entity, that generally means April 15. The exact date can shift for weekends and holidays, so confirm it for your own year. If your LLC does not use a December 31 year-end, that fourth-month deadline lands on a different date, so check the Form 1120 due date for your own tax year. If you need more time, you file Form 7004 by the deadline to get an automatic six-month extension of time to file, which also moves the Form 5472 due date.

For the step-by-step of preparing and sending that pro forma return, see our Form 1120 filing guide for foreign-owned LLCs. One practical point: a foreign-owned disregarded entity cannot e-file this pro forma return, so it is mailed or faxed to the IRS. Confirm the current mailing address and any labeling in the live IRS Instructions for Form 5472 before you send it. This article stays on who files, when, and what happens if you do not.

What is the penalty for not filing Form 5472?

The stakes are high, which is why this filing deserves attention even when no tax is owed. The penalty for failing to file Form 5472 on time, or for keeping incomplete records, is $25,000 for each required form, as the IRS Instructions for Form 5472 set out.

It does not stop there. If the failure continues more than 90 days after the IRS sends notice, a further $25,000 applies for each 30-day period, or part of one, that the failure goes on. The penalty is the same whether or not the LLC had any income.

What records should you keep for Form 5472?

The same $25,000 penalty reaches incomplete records, not just a missing form, so keep enough proof to support every related-party transaction you report. For each dealing between the LLC and its owner or another related party, hold on to:

The date, amount, and currency of the transaction, and who it was with.

Any agreement behind it, such as a loan note or a service contract.

Invoices, receipts, or bank records showing the money actually moved.

Your ledger or bookkeeping entries recording it.

These record-keeping duties sit in Treasury Regulation 1.6038A-3, and the live IRS instructions confirm what to retain. When in doubt, keep more rather than less.

Do you still file if the LLC had no income or owed no US tax?

Usually yes. This is the single most common misconception about Form 5472. It is a reporting requirement tied to related-party transactions, not a tax bill, so you can owe zero US tax and still be required to file.

A first-year LLC that you set up and funded, but that earned nothing, generally still has a reportable transaction, namely the funding itself. Whether your LLC actually owes any US tax is a separate question with its own rules, and it does not remove your duty to report.

Common Form 5472 filing mistakes to avoid

Assuming a no-income or first-year LLC has nothing to file, when funding it already triggers the requirement.

Treating Form 5472 as a tax return. It is an information return, filed on a pro forma Form 1120 that carries no corporate tax.

Missing the deadline because you did not realize it matches the Form 1120 due date, around April 15 for calendar-year filers.

Forgetting to file Form 7004 when you need more time, then filing the 5472 late.

Overlooking related-party dealings beyond sales, such as loans, contributions, and distributions between you and the LLC.

None of this is a substitute for advice on your own facts. If your ownership is shared, indirect, or spread across several entities, the 25% and related-party tests get more involved, and a qualified US tax professional can confirm how they apply to you.

What if you already missed a Form 5472 filing?

If you find a late or missed Form 5472, the safer move is usually to file the delinquent pro forma Form 1120 with Form 5472 as soon as you can, rather than leave it open. Filing does not erase a penalty by itself.

The law does let the penalty be reduced or removed where the failure was due to reasonable cause and not willful neglect, under section 6038A(d). That is a fact-specific request with no guaranteed outcome. A qualified US tax professional should help you prepare any reasonable-cause statement, and you should confirm the current procedure on the live IRS pages.

Frequently asked questions

Does a foreign-owned single-member LLC have to file Form 5472?

Yes, if it had a reportable transaction with a related party during the year. The IRS treats a wholly foreign-owned disregarded entity as a corporation for section 6038A, so it files Form 5472 attached to a pro forma Form 1120. Even funding the LLC from the owner counts as a reportable transaction.

Who is considered a 25% foreign owner for Form 5472?

A foreign person who owns at least 25% of the company by either total voting power or total value of all classes of ownership, at any time during the tax year, under IRC 6038A(c).

When is Form 5472 due?

It is due with the entity income tax return. For a foreign-owned LLC pro forma Form 1120, that is the 15th day of the 4th month after the tax year ends, about April 15 for calendar-year filers. You can get up to six more months by filing Form 7004.

What is the penalty for not filing Form 5472?

It is $25,000 per entity per year for failing to file on time or failing to keep the required records. If the failure continues more than 90 days after the IRS sends notice, a further $25,000 applies for each 30-day period that it goes on, under IRC 6038A(d).

Do I still file Form 5472 if my LLC had no income or owed no US tax?

Yes. Form 5472 is a reporting requirement tied to related-party transactions, not a tax bill. You can owe zero US tax and still be required to file, and the $25,000 penalty applies whether or not any tax was due.

What is the difference between Form 5471 and Form 5472?

They run in opposite directions. Form 5472 is filed by a foreign-owned US entity to report transactions with its related parties, while Form 5471 is filed by certain US persons who are officers, directors, or shareholders in a foreign corporation. A foreign-owned US LLC normally deals with Form 5472, but confirm your own facts against the IRS instructions.

How this article was prepared

The reporting corporation test, the treatment of a foreign-owned disregarded entity as a corporation for section 6038A, the reportable-transaction trigger, and the pro forma Form 1120 filing come from the IRS Instructions for Form 5472. The same source gives the $25,000 penalty and the continuation penalty after IRS notice. The 25% foreign shareholder definition, measured by voting power or value, comes from Internal Revenue Code section 6038A and Treasury Regulation 1.6038A-1. The record-keeping duties come from Treasury Regulation 1.6038A-3, and the reasonable-cause relief for penalties comes from section 6038A(d). The due date and the automatic six-month extension come from the IRS Instructions for Form 1120 and Form 7004. Last reviewed July 2026. This is general information, not legal or tax advice, and CORPBOLT is a formation service, not a law or accounting firm. Treat all IRS dates as the agency current figures, and confirm them on the live IRS pages before you file.

Get your foreign-owned LLC set up right with CORPBOLT: CORPBOLT forms and maintains Wyoming LLCs for non-residents from $349/year (Foundation), including the registered agent and US business address. The EIN your pro forma Form 5472 filing depends on is included from $599/year (Launch) or as a $199 add-on. We are a formation service, not a law firm or CPA, so a qualified tax professional should confirm your own filing duties. Form your Wyoming LLC →

Official references

IRS: Instructions for Form 5472 (who must file, reportable transactions, pro forma 1120, penalty)

Cornell LII: 26 U.S. Code 6038A (25% foreign shareholder, penalty)

Cornell LII: 26 CFR 1.6038A-1 (foreign-owned disregarded entity treated as a corporation)

Cornell LII: 26 CFR 1.6038A-3 (record maintenance for related-party transactions)

IRS: Instructions for Form 1120 (when to file, Form 7004 extension)

Approval note: Eligibility and approval decisions are made by each bank, fintech, and payment processor. Requirements can vary by provider, country, business model, and account history.