What is an LLC? An LLC, or Limited Liability Company, is a U.S. business entity formed under state law. It can separate business obligations from the owner's personal assets in many situations, while giving the owner flexible tax and management options. For non-US founders, an LLC is often used to create a U.S. operating entity, apply for an EIN, and keep formation documents organized. This page explains what an LLC is, how it works, where the limits are, and what documents usually matter after formation. It is general educational information, not legal, tax, or financial advice.

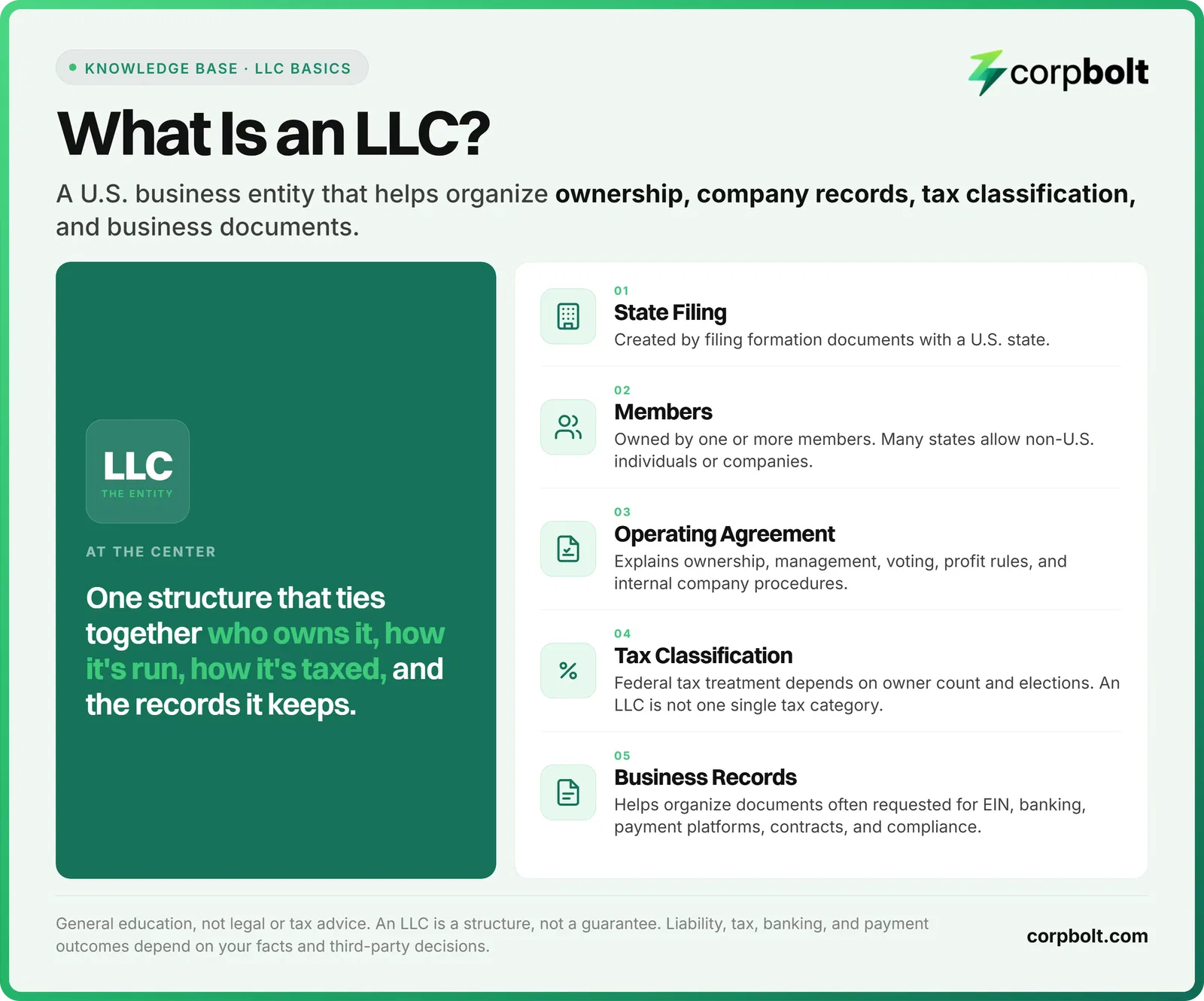

An LLC is a Limited Liability Company formed under U.S. state law.

It helps organize ownership, liability separation, tax classification, EIN steps, and company records.

An LLC does not guarantee liability protection, tax results, banking, payment processor approval, or platform acceptance.

What does LLC stand for?

LLC stands for Limited Liability Company. It is a business structure created by filing formation documents with a U.S. state. The IRS describes an LLC as a structure allowed by state statute, and each state can set its own rules for forming and maintaining one.

The owners of an LLC are called members. A member can be one person, several people, another company, or, in many states, a foreign individual or foreign entity. This is one reason LLCs are commonly considered by founders outside the United States who want a U.S. business presence.

What is an LLC and how does it work?

An LLC works by creating a registered business entity that is separate from its members for many business purposes. The LLC can usually enter contracts, receive payments, open business accounts, own business assets, and keep business records under its own name.

To form an LLC, a founder usually chooses a formation state, selects an available company name, appoints a registered agent, files Articles of Organization or a similar state document, and keeps internal records such as an operating agreement. Many LLCs also apply for an EIN from the IRS after formation.

If CORPBOLT helps with the formation, we prepare and submit filing information based on the details you provide. We do not choose the legal or tax structure for you, and we do not replace advice from a qualified attorney, CPA, or tax professional.

What does limited liability mean?

Limited liability means the LLC structure can help separate the company's debts and obligations from the personal assets of its members. The U.S. Small Business Administration explains that LLCs protect owners from personal liability in most instances. So personal assets such as your home, vehicle, or savings are usually not at risk only because the LLC faces a lawsuit or a debt.

In practice, your personal exposure is generally limited to what you put into the business. As Cornell Law School's Legal Information Institute puts it, an owner with limited personal liability usually cannot be sued personally to cover the company's liabilities, and may only lose the amount invested in the business. This is one of the main reasons non-resident founders form a U.S. LLC: it draws a clear line between you and the company. The protection is a general rule with limits, though, not a guarantee.

Can an LLC lose its liability protection?

Yes, in some cases. The protection is not absolute. A court can sometimes pierce the corporate veil and hold owners personally responsible for business debts. Cornell's Legal Information Institute notes that courts generally start with a strong presumption against doing this, and usually act only where there has been serious misconduct. Common warning signs courts may weigh include mixing personal and company money, leaving the business seriously underfunded, using the company to commit fraud, or treating it as a personal "alter ego" rather than a genuinely separate entity. No single factor is automatically decisive, and the rules vary by state and by court, so for a specific situation it is wise to speak with a qualified attorney.

How do you keep an LLC's liability protection?

Forming the LLC is only the first step. The shield generally holds up when you keep the company clearly separate from you personally. In practice, that comes down to a few habits:

Open a dedicated business bank account, and do not mix personal and company money.

Fund the business well enough to operate.

Put a written operating agreement in place, and keep it with your records.

Sign contracts in the company's name, not your own.

Keep basic company records.

These habits help the LLC read as its own legal person rather than an extension of its owner. None of it is a guarantee, but consistent housekeeping is usually what keeps the protection intact.

How is an LLC taxed?

An LLC is a state business entity, not a single federal tax category. The IRS generally treats a domestic single-member LLC as disregarded from its owner for income tax purposes unless it elects corporate treatment. A domestic LLC with two or more members is generally treated as a partnership unless it elects to be treated as a corporation.

This is why two LLCs can look similar on state records but file taxes differently. Some LLCs keep default tax treatment. Others file IRS Form 8832 to elect a different federal tax classification, or meet requirements to be treated as an S corporation. Tax classification can affect filings, owner reporting, employment taxes, and compliance work, so it should be reviewed with a qualified tax professional.

Here is how the main federal tax options compare for an LLC:

Federal tax treatment | When it applies | Main federal form |

|---|---|---|

Disregarded entity | Default for a single-member LLC | The owner reports the business on their own return (for a U.S. individual, usually Schedule C) |

Partnership | Default for a multi-member LLC | The LLC files Form 1065 and gives each member a Schedule K-1 |

C corporation | Optional, by filing Form 8832 | The LLC is taxed as a separate corporation (Form 1120) |

S corporation | Optional, by filing Form 2553, and only if the LLC is eligible | Pass-through with payroll rules; generally not available to LLCs with non-resident owners |

One detail trips up many single-member owners: being "disregarded" applies to income tax, not to everything. The IRS states that a single-member LLC treated as a disregarded entity for income tax is still a separate entity for employment tax and certain excise taxes. In practice that usually means the LLC itself, using its own name and EIN, handles those specific filings if you take on payroll or an excise-taxable activity. If that happens, confirm your obligations with a qualified tax adviser.

Timing also matters if you change your classification. On Form 8832, the IRS limits how you date the election. The effective date generally cannot be more than 75 days before, or 12 months after, the day you file. So you cannot backdate an election indefinitely. Once an entity elects to change its classification, it generally cannot change again for 60 months. If you miss a deadline, the IRS in some cases allows late-election relief when you request it within 3 years and 75 days of the intended effective date and meet the conditions.

Who owns and manages an LLC?

The owners of an LLC are called members. A single-member LLC has one owner. A multi-member LLC has two or more owners. Many states do not set a maximum number of members, and the IRS notes that members can include individuals, corporations, other LLCs, and foreign entities.

There are a few limits. The IRS notes that a few business types, such as banks and insurance companies, generally cannot be LLCs. And if your business provides licensed professional services, some states may require a professional LLC (a PLLC) rather than a standard one. The rules vary by state and profession, so it is worth confirming your situation before filing.

An LLC can be member-managed or manager-managed. In a member-managed LLC, the owners run the company directly. In a manager-managed LLC, the members appoint one or more managers to run daily operations. The operating agreement should describe how decisions are made, who can sign for the company, how profits are handled, and what happens if ownership changes.

What is an LLC used for by founders?

Founders often choose an LLC because it combines liability separation, flexible ownership, simpler management than a corporation, and possible pass-through tax treatment. The SBA also notes that business structure affects taxes, liability, paperwork, fundraising, and day-to-day operations.

For many non-US founders, a U.S. LLC can also make the business easier to present to U.S. customers, vendors, platforms, banks, and payment processors. An LLC does not guarantee banking, payment processor, marketplace, or tax outcomes, but it can provide the formal company records those third parties commonly ask to review.

What are the limitations of an LLC?

An LLC is flexible, but it is not the right fit for every situation, and it has trade-offs worth knowing before you file.

Self-employment tax is the first. By default, an active member's share of the profit is generally treated as self-employment earnings, which means it is usually subject to U.S. self-employment tax, the Social Security and Medicare portion. The IRS treats a single-member LLC owner much like a sole proprietor here, and members of a multi-member LLC taxed as a partnership generally pay it on their share too. Some owners look at an S-corporation election to manage this, but whether it helps depends heavily on your income, your role, and your home-country tax position, so it is genuinely fact-specific.

Changing ownership is the second. Moving ownership in an LLC is usually less straightforward than handing over corporate shares. Under most state LLC laws, transferring a membership interest does not by itself make the buyer a member. A transferee often receives only the economic share, unless the other members consent and the operating agreement allows it. Membership changes can also shift your tax status, since the IRS notes that a single-member LLC generally becomes a partnership once it adds a member. For owner-operated businesses this is rarely a problem, but founders planning to raise priced equity rounds often find a corporation a better fit.

What documents are usually connected to an LLC?

The exact documents depend on the state and the company's situation, but these are the common ones founders should understand:

Articles of Organization: The state filing that creates the LLC or records basic company details.

Registered agent record: The person or company designated to receive official legal and state notices.

Operating agreement: The internal document that explains ownership, management, voting, profit allocation, and company procedures.

EIN confirmation letter: The IRS confirmation for the company's Employer Identification Number, when an EIN is issued.

Annual report or state compliance filings: Ongoing state filings that may be required to keep the LLC in good standing.

For Wyoming LLCs, the Secretary of State's LLC Articles instructions list a $100 filing fee. They also require a registered agent with a physical Wyoming address, and state that annual reports are due each year on the first day of the anniversary month of formation. Wyoming is just one example - which state is actually right depends on where you operate and your tax position, which we cover in the best state to form an LLC for non-resident founders. Requirements can change, so always verify state instructions before relying on them.

Other states work differently, which is worth checking before you choose. Some charge an annual franchise tax or report fee on top of the filing fee. A few add a publication step. In New York, for example, a newly formed LLC is generally required, within 120 days, to publish notice of its formation in two county newspapers, once a week for six successive weeks. It then files proof with the state, and if it does not, its authority to do business in New York can be suspended. This is part of why many non-resident founders compare states carefully before they file.

Is an LLC the same as a corporation?

No. An LLC and a corporation are different business structures. Both can help separate owners from business liabilities, but they differ in ownership, management, tax treatment, fundraising mechanics, and corporate formalities.

An LLC is usually owned by members and managed under an operating agreement. A corporation is usually owned by shareholders and governed by directors, officers, bylaws, shares, and formal corporate records. A corporation can be better suited for certain investor-backed businesses, stock option plans, or plans to issue shares. An LLC is often simpler for owner-operated businesses, consultants, agencies, e-commerce founders, holding companies, and many service businesses.

Here is how the two structures compare on the points that matter most when you are choosing:

Comparison point | LLC | Corporation (C-corp) |

|---|---|---|

Owners are called | Members | Shareholders |

Default federal tax | Pass-through by default: profit is reported on the owners’ own tax returns (a single-member LLC is “disregarded”; a multi-member LLC is taxed as a partnership) | A C-corp is a separate taxpayer: it pays corporate income tax, and dividends paid out can be taxed again to shareholders (“double taxation”) |

Management | Members, or managers named in an operating agreement | A board of directors and officers, governed by bylaws |

Ownership units | Membership interests, with flexible profit splits | Shares of stock: supports option pools and multiple share classes |

Raising venture capital | Possible, but less standard for priced equity rounds | Preferred by most investors for priced rounds and stock options |

Formalities & records | Lighter: an operating agreement and fewer mandatory meetings | Heavier: bylaws, board and shareholder meetings, and minutes |

Common fit | Owner-operated businesses, consultants, agencies, e-commerce sellers, and holding companies | Investor-backed startups planning to issue stock or raise priced rounds |

One nuance the table simplifies: an LLC can elect to be taxed as an S-corporation or C-corporation by filing with the IRS, so “pass-through” is the default rather than a permanent rule. This is general information, not legal or tax advice. Confirm the right structure with a qualified professional. For a full side-by-side breakdown for non-US founders (including the S-corp election, state costs, and when converting makes sense), see LLC vs. Corporation: which is right for non-US founders?

How is an LLC different from a partnership?

The difference comes down to liability. In a general partnership, the partners are generally exposed personally, so their personal assets can in many cases be reached for business debts and lawsuits. A multi-member LLC is taxed like a partnership by default, so profit and loss generally pass through to the members, but unlike a plain partnership it adds the liability shield described above. That mix of pass-through tax with a liability separation, plus lighter formalities than a corporation, is a big part of why many non-resident founders choose an LLC.

Is an LLC right for non-US founders?

An LLC can be a strong option for non-US founders who want a U.S. entity, especially when they need a registered company, an EIN, and organized business documents. The IRS states that most states do not restrict LLC ownership, and members may include foreign entities. That does not mean every non-US founder should use the same structure.

Your tax residence, customer location, business activity, payment processor needs, U.S. source income, treaty position, and reporting obligations can all affect whether an LLC is the right choice. If your situation involves cross-border tax, employees, partners, investors, or physical U.S. operations, get professional advice before making the final decision.

What should you do after forming an LLC?

After formation, the next step is usually document cleanup and compliance setup. A useful post-formation checklist includes:

Confirm the Articles of Organization were accepted by the state.

Save the formation receipt and stamped state documents.

Prepare or review the operating agreement.

Apply for an EIN if the business needs one.

Keep business money and personal money separate.

Track annual report, registered agent, address, and tax deadlines.

Store key documents somewhere easy to access before applying for banking, payment processing, or marketplace accounts.

If you are forming from outside the US, the full step-by-step formation guide for non-residents walks through the whole process. CORPBOLT helps founders organize formation documents, EIN filing steps, and bank-ready company records based on the plan selected. Third-party approvals still depend on the bank, platform, payment processor, government agency, and the information you submit.

This is often the stage where good guidance matters most:

Quick FAQ

Can one person own an LLC?

Yes. Most states allow single-member LLCs, which means one person or entity owns the company. For federal income tax purposes, a domestic single-member LLC is generally disregarded as separate from its owner unless it elects corporate tax treatment.

Can a non-US resident own a U.S. LLC?

In many cases, yes. The IRS notes that LLC members may include foreign entities, and many states allow non-US individuals or companies to own LLCs. The harder question is usually tax reporting, banking, payment processing, and compliance, not basic ownership.

Does an LLC automatically get an EIN?

No. Forming an LLC with a state does not automatically issue an EIN. An EIN is handled by the IRS. Some LLCs need an EIN for tax, banking, hiring, payment processor, or marketplace reasons. Others may need professional guidance before applying.

Does an LLC guarantee banking or payment processor access?

No. An LLC can provide important company documents, but banking and payment processor decisions are made by third parties. They may review your owners, business model, address, documents, website, industry, country, and risk profile.

Is an LLC legal advice or tax advice?

No. This article is general education. Choosing an entity and tax classification can have legal, tax, and compliance consequences. CORPBOLT can help with administrative formation steps, but it is not a law firm, CPA firm, tax advisor, or financial institution.

Does an LLC fully protect my personal assets?

Not fully. An LLC protects owners from personal liability in most instances, but the protection is not absolute. In some cases a court can pierce the corporate veil and reach personal assets, usually where there has been serious misconduct such as mixing personal and company funds or fraud. Keeping the company genuinely separate, with its own bank account and records, is what helps preserve the shield.

Does a single-member LLC need its own EIN to hire employees?

Generally, yes. Even when a single-member LLC is "disregarded" for income tax, the IRS treats it as a separate entity for employment taxes, so it uses its own name and EIN to report and pay payroll taxes. If you plan to hire, set up the EIN first.

Official references

How this article was prepared

Summary: CORPBOLT prepared this guide as customer education for founders researching U.S. LLCs. It is based on official IRS, SBA, and state source material, then reviewed for source alignment, plain-English clarity, non-US founder relevance, and unsupported claims about liability, taxes, EINs, banking, payment processors, or third-party approvals.

Primary sources: IRS LLC, single-member LLC, and tax classification guidance; IRS Publication 3402; SBA business structure guidance; Cornell Law School's Legal Information Institute on limited liability and veil-piercing; and relevant state filing rules.

Review checks: Definition accuracy, source alignment, practical founder usefulness, claim safety, and clear boundaries around legal, tax, banking, and payment outcomes.

Last reviewed: June 2026. This article is updated when official source material, product workflows, or compliance expectations change.

Forming one with CORPBOLT: CORPBOLT forms your Wyoming LLC with a U.S. business address from $349/year; Launch ($599) adds the EIN and a digital mailbox. See how CORPBOLT does this →

Important: This article is for general information only and is not legal or tax advice. Requirements can vary by state, provider, and individual circumstances, so consider speaking with a qualified legal or tax professional before making filing, tax, banking, or payment decisions. Eligibility and approval decisions are made by each bank, fintech, and payment processor.