Yes, a non-resident who owns or is forming a Wyoming LLC can open a US business bank account. There is no Wyoming-bank requirement and no guaranteed approval. You prepare a bank-ready file, and each bank decides.

Banks typically ask for the EIN, the filed Articles of Organization, an operating agreement, your passport, an address, and owner details.

Acceptance is each bank's own Customer Identification Program decision under federal rules, not a legal right you can demand.

A Wyoming LLC can bank with any US bank or online-first provider, since account location follows bank policy.

What a bank is actually deciding (and what it is not)

It helps to understand what happens when you apply. A bank is not checking whether your Wyoming LLC has a right to an account. It is running its own onboarding checks and deciding whether to accept you. That distinction shapes everything below.

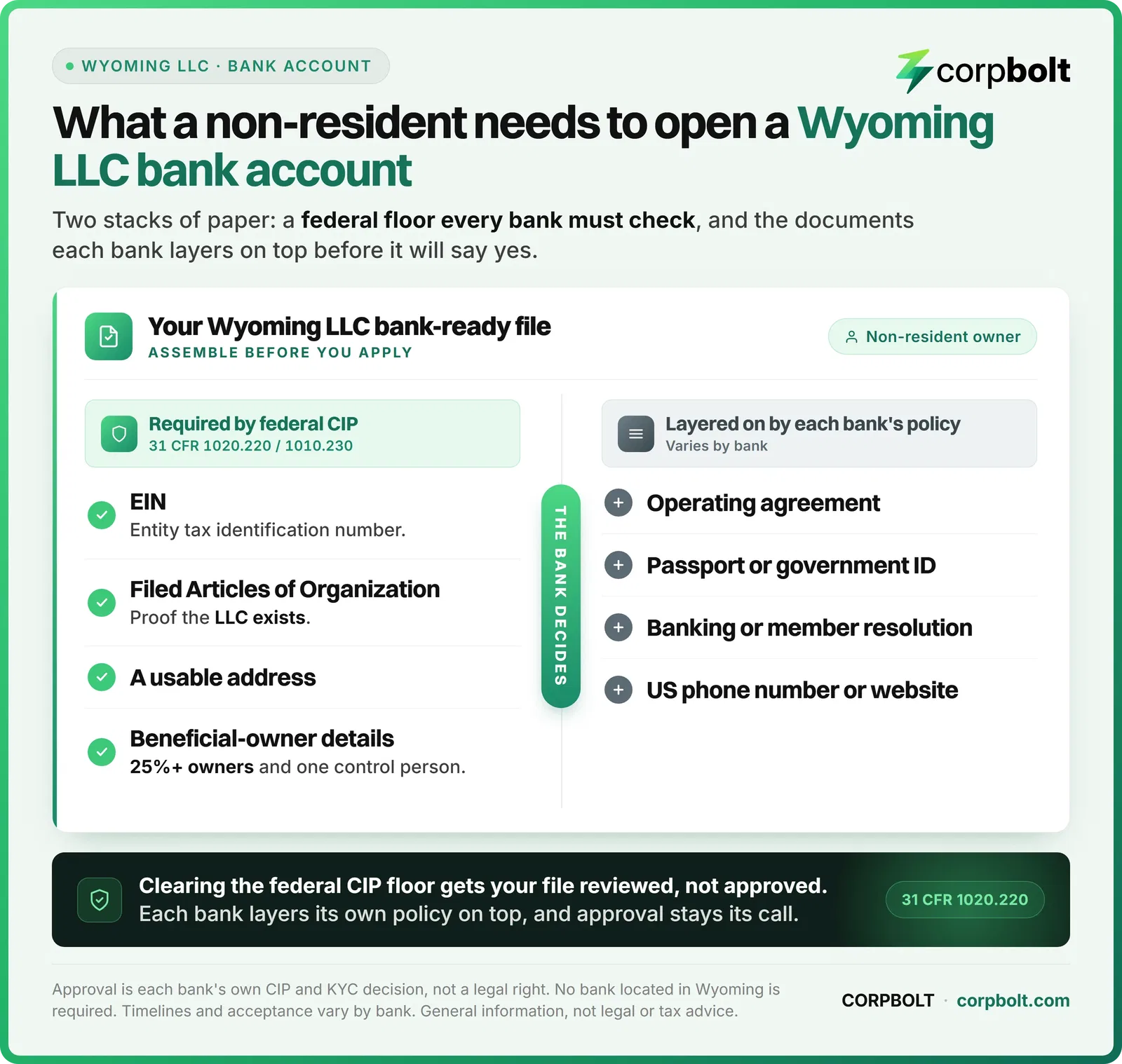

Federal law requires every US bank to run a written Customer Identification Program, or CIP. The rule at 31 CFR 1020.220 says the program must use risk-based procedures that let the bank form a reasonable belief it knows the true identity of each customer. This is a duty the bank owes the government. It does not entitle any applicant to an account.

So most "bank requirements" you read about are bank policy, not law. A non-resident owner (see our guide on the Wyoming LLC for non-residents) can prepare a strong file and still be declined by one bank and accepted by another. CORPBOLT sits on the preparation side of that line. We help you obtain the EIN and make your documents bank-ready, but we do not open accounts or guarantee approval.

The documents and information a bank typically asks for

Most banks want the same core file from a non-resident Wyoming LLC. Some pieces trace directly to the federal CIP minimum. Others are individual bank policy layered on top of that floor. The table below separates the two so you know what is baseline and what varies.

Document or information | What it shows the bank | Basis |

|---|---|---|

EIN (entity tax ID) | The LLC's federal identification number | Identification number, a CIP minimum |

Filed Articles of Organization | That the LLC legally exists | Entity-existence document, a CIP minimum |

Operating agreement | Who owns and runs the LLC | Bank policy on top of the floor |

Passport or government ID | Your identity as an owner | Individual identity, bank policy |

A usable address | Where the business or owner is located | Address, a CIP minimum |

Beneficial-owner details | Who owns 25% or more and who controls it | Beneficial ownership, 31 CFR 1010.230 |

Banking or member resolution | That the LLC authorized opening the account | Bank policy |

US phone number or website | Contact details and business activity | Bank policy, often online-first providers |

The federal floor is narrow. 31 CFR 1020.220 lists the minimum CIP elements as name, address, and an identification number. For an entity, it adds documents showing the entity exists, such as certified articles. Everything past that, like a certified operating agreement or a signed resolution, is a policy choice by the individual bank.

Who signs the resolution. If a bank asks for a banking resolution or a signature card, it needs to see that the person opening the account is authorized to act for the LLC. Check your operating agreement first: a Wyoming LLC is member-managed by default and manager-managed only if the articles or the operating agreement say so, under Wyoming Statute 17-29-407. Management authority sits with the members in a member-managed LLC and with the managers in a manager-managed one, so the resolution should name the authorized signer and their role to match that structure.

The filed formation paperwork does most of the heavy lifting here. If you want a full picture of what arrives once your LLC is approved, see the documents you receive after forming an LLC.

Some banks also ask for proof that your LLC is currently active with the state. That is a separate document you can request when needed; our guide to the Wyoming certificate of good standing explains what it is and how to get one. Not every bank asks for it.

The federal CIP floor versus each bank's own policy layer.

The EIN: the practical prerequisite, and how to get one without an SSN

An EIN is the piece most banks treat as non-negotiable. It is typically required to open a US business account, though that is a bank and CIP norm rather than a statute. The IRS itself recognizes the use case: Form SS-4 lists "Banking purpose" as a valid reason to apply on line 10. If a bank later asks you to prove the EIN, your IRS confirmation records are what you show; our guide to the CP 575 EIN confirmation letter covers how to get or replace one.

If you have no SSN or ITIN, you can still get one. According to the IRS Instructions for Form SS-4, applicants with no legal US residence or principal place of business cannot use the online application. You file instead by phone at 267-941-1099, or by fax or mail. When the responsible party has no SSN or ITIN and is ineligible for one, you enter "foreign" on line 7b.

We do not promise an IRS turnaround. Timing is set by the IRS, not by us, so verify current processing on the live IRS page. For a deeper walkthrough of the number itself, read what an EIN is.

Beneficial-owner information the bank collects

Banks do not just identify the LLC. Under 31 CFR 1010.230, a covered bank must identify and verify the beneficial owners of a legal entity customer at account opening. That means two prongs. The ownership prong covers each individual who owns 25% or more of the equity. The control prong covers one individual with significant responsibility to control or manage the LLC.

The bank may rely on the beneficial-owner information the LLC supplies, unless it has reason to think that information is unreliable. This is the bank's own onboarding step. It is separate from any federal beneficial-ownership reporting you may owe elsewhere.

The address question, and why you do not need a Wyoming bank

A bank must collect an address as part of its CIP. That is a firm requirement in 31 CFR 1020.220. What is not fixed by law is which kind of address a given bank will accept. Whether a registered-agent address or a US mail-forwarding address passes is that bank's own policy, not a statute.

So do not assume any particular address type will be approved. Some banks accept a forwarding or agent address, and others want something else. If you are still sorting out an address, our note on a free virtual address for an LLC covers the options and the tradeoffs.

One myth worth killing early: you do not need a bank located in Wyoming. Nothing in the CIP rule or the Wyoming LLC Act ties account eligibility to your state of formation. Account location follows bank policy, not the state where you filed.

Opening remotely versus in person

Many non-residents ask whether they must fly to the US. Legally, remote opening is permitted. The CIP rule lets a bank verify identity through documents, non-documentary methods, or a combination of both. That combination is what makes remote onboarding possible.

But permitted is not the same as required. No rule forces a bank to accept a remote or non-resident applicant. Some providers onboard foreign-owned LLCs entirely online. Others want physical presence at a branch. Treat this as bank-by-bank variance and plan for both outcomes.

The account-opening workflow, step by step

Once your file is ready, opening an account follows a predictable sequence. Treat the steps below as a preparation-side workflow, not a promise of approval, since each bank still makes its own decision.

Get the EIN issued first. Most banks will not open an account without it, so obtain the EIN before you apply; the EIN section above covers how a non-resident files.

Reconcile your entity and owner details. Check that the LLC name, the address, and owner information match across the filed Articles, the EIN paperwork, your ID, and the operating agreement. Banks flag mismatches during their identity checks.

Confirm the provider onboards your situation. Before you apply, check whether the bank accepts foreign-owned LLCs and remote applicants, since neither is guaranteed and policies vary bank by bank.

Submit the complete file. Send the full file from the table above as one package.

Respond to follow-up requests. A bank running its Customer Identification Program may ask for supplemental documents or clarification. Answering promptly keeps the review moving.

Why approval is never guaranteed

Applications stall or get declined for reasons that sit inside the bank's risk appetite. A bank may be unfamiliar with foreign-owned LLCs. It may treat certain industries as high-risk. It may want a deposit level you cannot meet yet, or it may simply find the file incomplete.

None of these are things a preparation service can override. CORPBOLT can make your file complete and consistent. It cannot change a bank's CIP decision, and it will not promise you an outcome.

Why a dedicated business account matters

Keeping business money separate is not just tidy bookkeeping. It is tied to the liability shield you formed the LLC for. Wyoming law is explicit that a limited liability company is an entity distinct from its members, under Wyoming Statute 17-29-104. That separateness is the whole basis for keeping the two pots of money apart.

Wyoming Statute 17-29-304 goes further. It says LLC debts do not become a member's or manager's debts solely by their status. But it also lists factors a court weighs when deciding whether to pierce that shield. One named factor is intermingling of the assets, operations, and finances of the company and the members to the point there is no distinction between them.

Read plainly, commingling business and personal money is a documented risk factor, not a neutral habit. A dedicated account is primary-source-backed liability hygiene. It is one of the cleaner ways to keep that distinction visible.

Frequently asked questions

Do I need an SSN or ITIN to open a US bank account for my Wyoming LLC?

No. The LLC's EIN identifies the entity and your passport or foreign government ID identifies you, so an SSN or ITIN is not needed to form the LLC, and many providers do not require one to open. Per the IRS, a foreign responsible party is not required to have an SSN or ITIN to obtain the EIN. No specific bank's acceptance is promised.

Can my Wyoming LLC have a bank account in its own name?

Yes. A Wyoming LLC is a legal entity distinct from its members under Wyoming Statute 17-29-104, so once a bank accepts the application the account is opened and held in the LLC's own legal name, not in your personal name. That is different from a member's personal account: keeping the company's money in the entity's own account is what maintains the separation between business and owner. Approval still rests with each bank.

Does my Wyoming LLC need a bank located in Wyoming?

No. You can bank with any US bank or online-first provider regardless of where you formed. Account eligibility is set by each bank's policy, not by your state of formation. Nothing in the federal CIP rule ties an account to the formation state.

Can I open the account without traveling to the US?

Sometimes. Federal law allows identity verification by non-documentary methods, which makes remote opening legally permissible. Whether a bank accepts remote or non-resident applicants is that bank's own CIP policy. There are no named providers here and no guarantee.

Will CORPBOLT open the account or guarantee approval?

No. CORPBOLT prepares bank-ready documents only. Opening and approving the account is each bank's CIP and KYC decision under 31 CFR 1020.220. We cannot promise approval or a timeline.

How long does it take to get the EIN and open an account?

We do not promise a turnaround. Timing sits with the IRS and then the bank. Verify current IRS processing on the live IRS page before you plan around a date.

How this article was prepared

The EIN filing route for a non-resident with no SSN maps to the IRS Instructions for Form SS-4. The CIP requirements, the identity and address minimums, and the remote-verification point map to 31 CFR 1020.220. The beneficial-owner rules map to 31 CFR 1010.230. The separate-entity and veil-piercing points map to Wyoming Statutes 17-29-104 and 17-29-304. The management-authority point for who signs a banking resolution maps to Wyoming Statute 17-29-407. Last reviewed July 2026. This is general information and not legal or tax advice. CORPBOLT is a formation service, not a law or accounting firm. Any IRS or bank figure here is the agency's current position to verify on the live page.

Bank-ready with CORPBOLT: CORPBOLT forms and maintains Wyoming LLCs for non-residents from $349/year (Foundation), including the registered agent and annual upkeep. The EIN is included from $599/year (Launch) or as a $199 add-on. Form your Wyoming LLC →