Generally no. A foreign-owned U.S. single-member LLC does not complete Schedule G on the pro forma Form 1120 it files with Form 5472. The IRS says that pro forma return needs only the entity's name and address plus items B and E.

The Form 5472 instructions list only name, address, and items B and E as required, so Schedule G is never reached.

Schedule G's 20% and 50% voting-stock thresholds are not the same as Form 5472's separate 25% foreign-owner test.

Your exposure is the Form 5472 penalty, currently $25,000, not any Schedule G penalty.

If you searched for "Form 1120 Schedule G" while getting a foreign-owned Wyoming LLC compliant, you likely hit a wall of preparer jargon. This page cuts to what matters for you. In almost every case, you never touch Schedule G. Below is why, plus the number trap that sends people here in the first place.

What Schedule G (Form 1120) actually is

Schedule G is an attachment to Form 1120, the U.S. corporate income tax return. Its official title is "Information on Certain Persons Owning the Corporation's Voting Stock," per the IRS form itself. Its job is narrow. It identifies certain owners of a corporation's voting stock so the IRS can see who controls the company. A corporation completes and attaches it only when it files a real Form 1120 and meets the ownership test described further down. For a typical foreign-owned LLC, that situation does not arise.

Why your foreign-owned LLC never reaches Schedule G

The answer comes from how your entity is taxed. By default, a single-member LLC is a disregarded entity for income tax purposes. The IRS treats it as not separate from its owner, so it files no income tax return of its own. Its activity is reflected on the owner's return instead.

A foreign-owned U.S. disregarded entity still carries one reporting duty. Under the section 6038A regulations, it must file a pro forma Form 1120 with Form 5472 attached by the 1120 due date, including extensions. The IRS defines a foreign-owned U.S. disregarded entity as a domestic entity that is wholly owned by a foreign person.

The phrase "pro forma" is doing the heavy lifting here. This 1120 is near-empty. The IRS instructions for Form 5472 (current revision, verified July 2026) state that the only information required on it is the entity's name and address plus items B and E on the first page. You also write "Foreign-owned U.S. DE" across the top. That is the whole return.

You file the pro forma 1120 and Form 5472 together by mailing them to the IRS at 1973 Rulon White Blvd, M/S 6112, Ogden, UT 84201, or by faxing them. The current Form 5472 instructions give the fax number as 855-887-7737, and require the fax to be sent at 300 DPI or higher. Because Schedule G is not on the short list of required items, it is simply never completed on this return.

The 20% and 50% versus 25% number trap

Most people who search for Schedule G do so because two forms use ownership percentages, and the numbers get tangled. Getting this straight is the point of the whole article.

The Schedule G form sets its own thresholds. It reaches any owner that owns directly 20% or more, or owns directly or indirectly 50% or more, of the total voting power of the corporation's stock. So the Schedule G trigger is 20% or 50%, not 25%.

On Form 1120 itself, Schedule K, Question 4 is labeled "Constructive Ownership of the Corporation." That question directs a corporation to complete and attach Schedule G when the 20% or 50% test is met. The 25% figure many readers arrive with is a different number entirely. It belongs to Form 5472's separate test for a 25% foreign owner. Neither number means you complete Schedule G on a pro forma 1120.

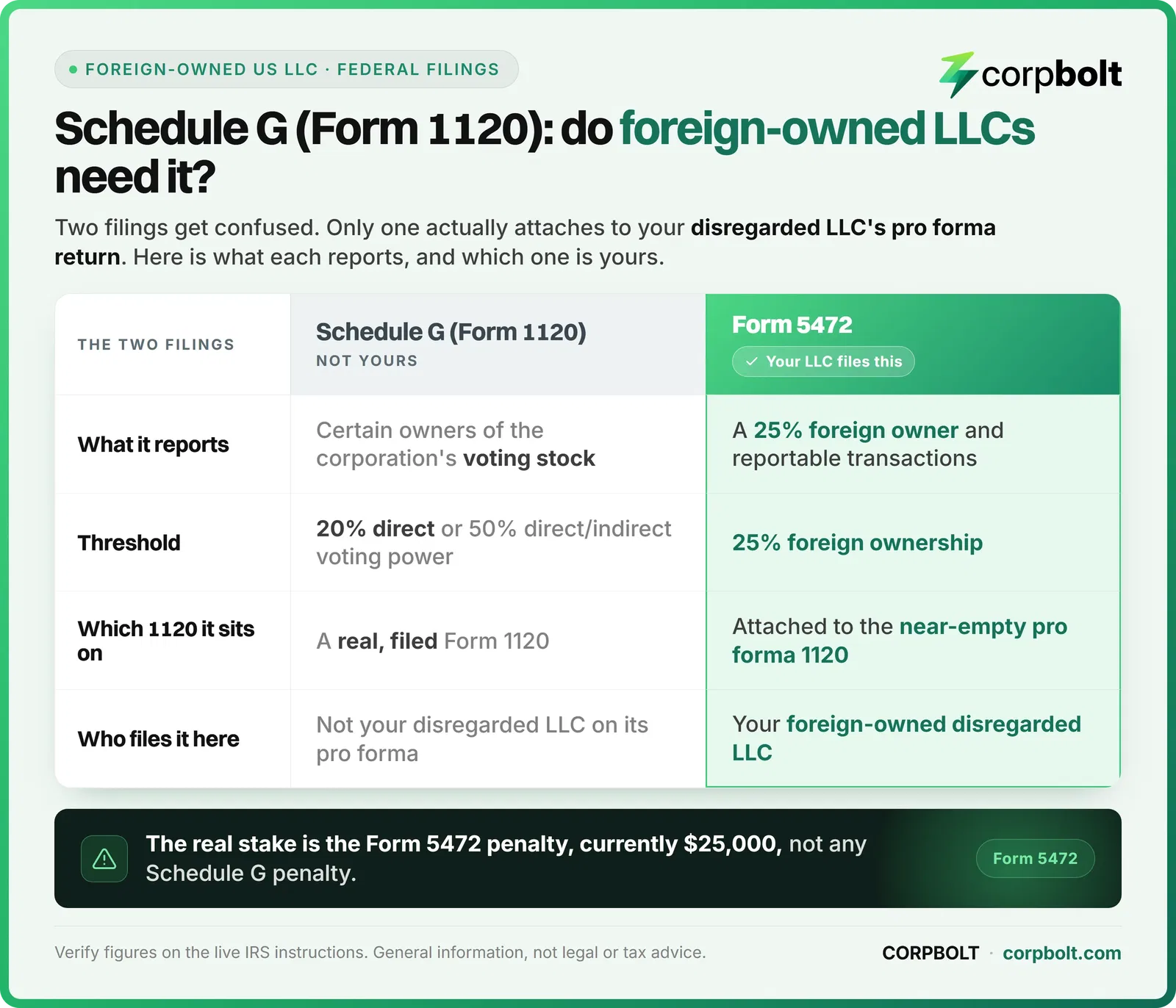

Schedule G versus Form 5472 at a glance

Here is the same distinction laid out side by side, so you can see why one form applies to you and the other does not.

Schedule G versus Form 5472: which one a foreign-owned LLC files.

Point | Schedule G (Form 1120) | Form 5472 |

|---|---|---|

What it reports | Certain owners of the corporation's voting stock | A 25% foreign owner and reportable transactions |

Threshold | 20% direct or 50% direct or indirect voting power | 25% foreign ownership |

Which 1120 it sits on | A real, filed Form 1120 | Attached to the near-empty pro forma 1120 |

Who files it here | Not your disregarded LLC on its pro forma return | Your foreign-owned disregarded LLC |

Read across the "Which 1120 it sits on" row and the reason clicks into place. Schedule G lives on a real corporate return. Your Form 5472 rides on a pro forma one. They almost never meet on the same filing.

The one edge case where a real 1120 appears

There is a single boundary worth naming plainly. A foreign-owned single-member LLC only files a real, non-pro-forma Form 1120 if it affirmatively elects to be treated as a corporation by filing Form 8832. That is not the default path for a Wyoming disregarded LLC. The default, as covered above, is disregarded status with a pro forma return.

If an entity did make that election, it would file a regular Form 1120, and it could reach Schedule G only if it actually met the 20% or 50% ownership test. In that case, Schedule G splits its disclosure into two sections: Part I covers qualifying organization owners, such as a corporation, partnership, trust, or tax-exempt organization, and Part II covers qualifying individual and estate owners, per the Schedule G form and the Instructions for Form 1120. See the IRS Schedule G (Form 1120) for the fields each part requires. That is a different tax posture from the one this page addresses. A separate corporate return, Form 1120-F, applies to certain foreign corporations rather than to a domestic disregarded LLC. For a non-resident running a straightforward Wyoming LLC, the disregarded default is the usual route, and Schedule G stays out of reach.

The real stake: the Form 5472 penalty

If there is a compliance risk here, it is not a Schedule G risk. It is the penalty for missing Form 5472.

The Form 5472 instructions (current revision, verified July 2026) state that a $25,000 penalty is assessed on any reporting entity that fails to file Form 5472 when due. If the failure continues for more than 90 days after the IRS mails notice, an additional $25,000 penalty applies for each 30-day period, or part of a period, that the failure continues. The takeaway is simple. Get Form 5472 and its pro forma 1120 filed on time, and Schedule G stays a non-issue. If you need the full filing steps, our guide to Form 5472 and the pro forma 1120 walks through the whole workflow.

Frequently asked questions

Is Schedule G required for Form 1120?

On a regular Form 1120, Schedule G is required when the corporation answers "Yes" to Schedule K, Question 4a or 4b, the constructive-ownership questions. That is the case when an owner holds directly 20% or more, or directly or indirectly 50% or more, of the corporation's voting power, per the Schedule G form and the Instructions for Form 1120. A foreign-owned U.S. single-member LLC is the exception. It files only a pro forma Form 1120 with Form 5472, which the IRS Form 5472 instructions limit to the entity's name and address plus items B and E, so it never reaches Schedule G.

How do I fill out Schedule G on Form 1120?

If you run a foreign-owned single-member LLC on the default disregarded path, you do not fill out Schedule G at all. Your pro forma Form 1120 is limited to the entity name, address, and items B and E, so there is no Schedule G to complete. Schedule G only comes into play on a regular, filed Form 1120 — when the corporation answers "Yes" to Schedule K, Question 4a or 4b. In that situation you complete Part I for organization owners and Part II for individual and estate owners, following the field order on the IRS Schedule G (Form 1120) form and the Instructions for Form 1120. This page stops at that boundary, because it does not apply to the disregarded LLC most non-resident founders run.

Is Schedule G the same as, or filed with, Form 5472?

No. Form 5472 reports a 25% foreign owner and reportable transactions, and a foreign-owned disregarded LLC attaches it to a near-empty pro forma Form 1120. Schedule G reports certain 20% or 50% voting-stock owners on a real, filed Form 1120. Per the Form 5472 instructions and the Schedule G form, Schedule G is not completed on the pro forma 1120 you attach to Form 5472.

What actually goes on the pro forma Form 1120 for a foreign-owned LLC?

Per the IRS Form 5472 instructions, the only information required is the entity's name and address plus items B and E on page 1. You also write "Foreign-owned U.S. DE" across the top of the form. Nothing else is required, and that includes Schedule G.

What happens if I skip the Form 5472 filing?

The Form 5472 instructions set a $25,000 penalty for failing to file Form 5472 when due, with a further $25,000 for continued failure after IRS notice. This penalty, not any Schedule G penalty, is the real stake for a foreign-owned LLC.

How this article was prepared

The rule that a foreign-owned disregarded LLC completes only name, address, and items B and E on the pro forma 1120 is drawn from the IRS Instructions for Form 5472. So are the "Foreign-owned U.S. DE" label, the Ogden filing address and fax, and the $25,000 penalty. Schedule G's title and its 20% and 50% voting-power thresholds come from the Schedule G form. The Schedule K Question 4 constructive-ownership routing is from the Instructions for Form 1120. The default disregarded-entity treatment and the Form 8832 corporate election are from the IRS single-member LLC page. Last reviewed in July 2026 by Charles Morente, Formation Specialist at CORPBOLT. This is general information and not legal or tax advice, and CORPBOLT is a formation service, not a law or accounting firm. Any fee, penalty amount, address, or date is the IRS's current figure to verify on the live page.

Filing your Wyoming LLC compliance with CORPBOLT: CORPBOLT forms and maintains Wyoming LLCs for non-residents from $349/year (Foundation), including the registered agent and annual report upkeep. The EIN is included from $599/year (Launch) or as a $199 add-on. Form your Wyoming LLC →