Form 1120 is the IRS U.S. Corporation Income Tax Return, the annual return a C corporation files to report its income and figure its tax. If you own a foreign-owned single-member LLC that is a disregarded entity, you almost never file that real return. Instead you file a near-empty pro forma Form 1120 as a cover sheet for Form 5472, and it carries no corporate tax.

It reports income, gains, losses, deductions, and credits, and figures a corporation's income tax. A default LLC does not compute corporate tax this way.

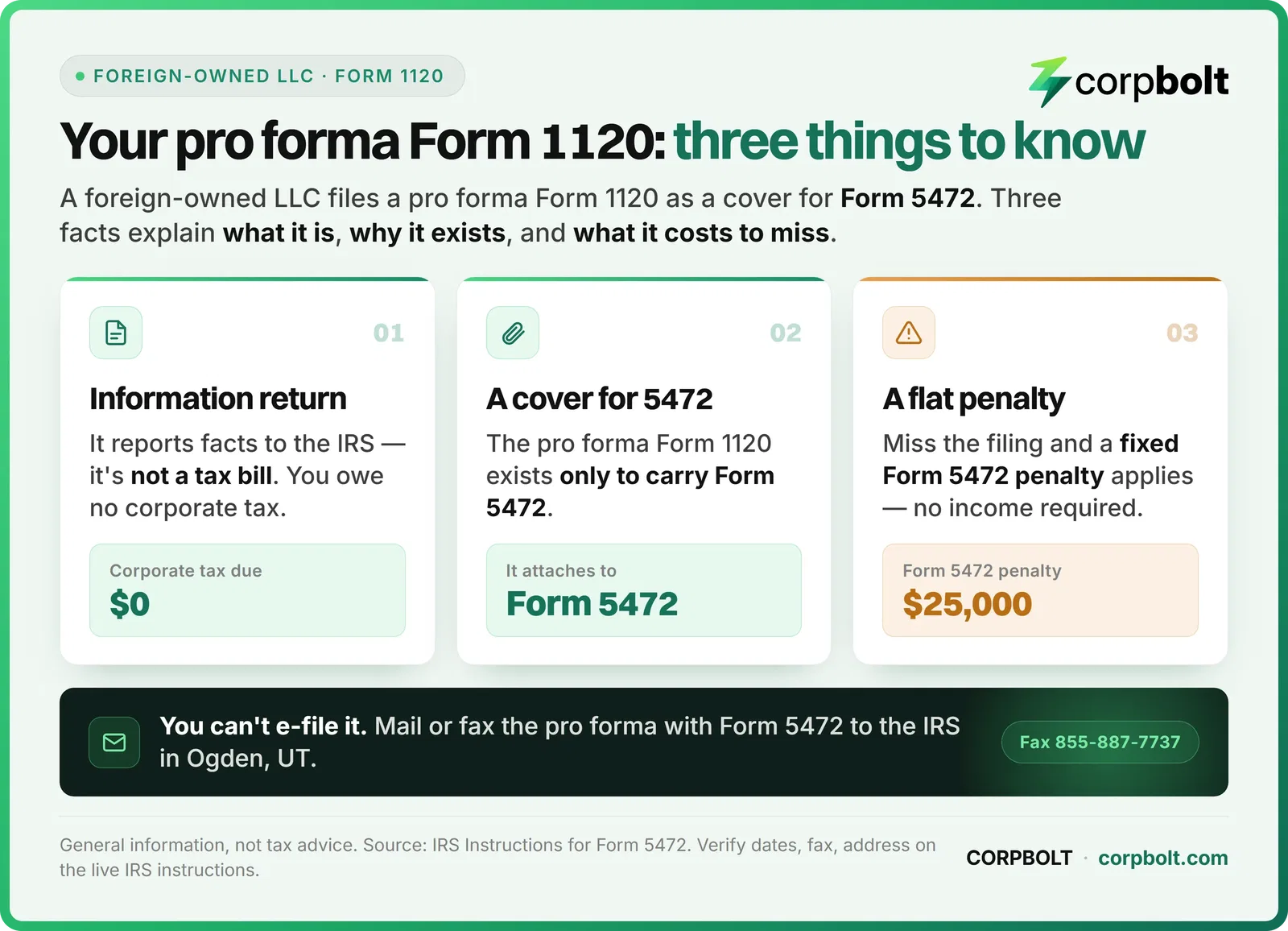

Under the section 6038A rules, a foreign-owned U.S. disregarded entity files a near-empty Form 1120 purely to carry Form 5472. It owes no income tax.

You mail or fax the package to a dedicated IRS unit. The load-bearing risk is a flat 25,000 dollar Form 5472 penalty, not a corporate tax bill.

What Form 1120 actually is

Form 1120 is officially titled the U.S. Corporation Income Tax Return. A domestic corporation uses it to report its income, gains, losses, deductions, and credits, and to figure its income tax liability. It is a real tax return, with dozens of lines and supporting schedules. That is the document the search results usually describe, and for most corporations it is exactly right.

But it is probably not the document you came here to file. If you own a foreign-owned U.S. LLC, the words Form 1120 point to a very different, much simpler filing. We get to that below.

Who normally files a real Form 1120

The ordinary filer is a taxpaying domestic corporation. The IRS instructions are blunt: unless exempt under section 501, all domestic corporations must file an income tax return whether or not they have taxable income. A domestic entity that elects to be taxed as a corporation files Form 1120 and attaches Form 8832.

These corporations owe corporate income tax because of how they are taxed. The IRS explains that a corporation's profit is taxed to the corporation when earned, then taxed again to the shareholders when it is paid out as dividends. That double tax defines the normal Form 1120 filer. It is also why a real return computes tax that you, as a disregarded LLC owner, may not owe at all.

Why your Wyoming LLC probably does not file a real 1120

By default, a single-member LLC is a disregarded entity, not a corporation. The IRS treats it as separate from its owner only if it files Form 8832 and affirmatively elects corporate treatment. Left alone, the LLC files no separate income tax return, and the owner reports its activity on their own return.

So there is no corporate tax computation to put on a real Form 1120. A genuine income-tax Form 1120 would apply only if you elected corporate taxation, which is a deliberate step, not the default. For most non-resident founders on a plain Wyoming LLC, that election never happens, and the real return never applies.

The pro forma Form 1120: the version you actually file

Here is the version that applies to you. Final regulations under section 6038A changed the rules for tax years beginning on or after January 1, 2017. Since then, a foreign-owned U.S. disregarded entity is treated as a corporation for the limited purpose of information reporting.

That means your LLC has no income tax return to file, yet it must file a pro forma Form 1120 with Form 5472 attached. Pro forma means for the sake of form: the 1120 is a near-empty cover sheet, and Form 5472 is the actual information return riding on top of it. Our guide to Form 5472 and the pro forma Form 1120 covers that reporting form in depth.

This is an information return, not a tax bill. You are reporting transactions, not paying corporate income tax. The table below shows how far apart the two documents really are.

How they compare | Real Form 1120 | Pro forma Form 1120 |

|---|---|---|

Who files | A taxpaying domestic corporation | A foreign-owned disregarded LLC |

What you complete | The full line-by-line return plus schedules | Name and address, plus items B and E |

Corporate tax owed | Income tax on the corporation's profit | Zero, it is an information return |

How you file | Electronically or on paper | Mail or fax only, never e-filed |

Governing rule | Income tax return | Section 6038A information reporting |

If you miss it | Regular late-return penalties | Flat 25,000 dollars Form 5472 penalty |

What you actually complete

On the pro forma Form 1120, you complete very little. The IRS Instructions for Form 5472 say the only information required is the name and address of the disregarded entity, plus items B and E on the first page. You write Foreign-owned U.S. DE across the top of the form, and you leave the rest blank.

Item B is the employer identification number box, so your LLC needs an EIN before it can file. You can get that EIN without a Social Security number. On Form SS-4 you check the Other box on line 9a and write Foreign-owned U.S. disregarded entity-Form 5472. If the responsible party has no U.S. tax ID and cannot get one, you enter foreign or N/A on line 7b.

Because the pro forma return stays blank, the usual schedules do not apply the way they would on a real return. If you are unsure whether a specific one is needed, see our note on Schedule G for foreign-owned LLCs. For the full walkthrough, follow our Form 1120 filing guide instead of piecing it together here.

How and where you file it

This package cannot be e-filed. The Instructions for Form 5472 require the disregarded entity to send it on paper, to a dedicated unit, not the standard Form 1120 addresses. You fax it to 855-887-7737, or mail it to Internal Revenue Service, 1973 Rulon White Blvd, M/S 6112, Attn: PIN Unit, Ogden, UT 84201.

Treat that fax number and address as the IRS's current channel. Confirm both on the live IRS Instructions for Form 5472 before you send anything.

Deadline and extension

The pro forma Form 1120 is due by the normal Form 1120 due date, including extensions. For a calendar-year LLC, that is the 15th day of the fourth month after year-end, generally April 15, per the Instructions for Form 1120. The exact date shifts for weekends and holidays, so verify it for your own year.

Need more time? You file Form 7004 by the due date to request an automatic extension. You enter the Form 1120 code in Part I, line 1, and you write Foreign-owned U.S. DE across the top, just as you do on the 1120 itself.

The trigger and the 25,000 dollar stakes

You might assume a dormant, no-income LLC has nothing to file. Usually that is wrong. The filing is triggered by a reportable transaction with a related party, and for a foreign-owned disregarded entity that expressly includes forming and funding the LLC, plus any distributions back to you.

So a first-year LLC that you simply set up and put money into generally has a reportable transaction, and a filing duty, even with no revenue at all.

Where this filing goes wrong

Trying to e-file the package. It must go by mail or fax.

Using a standard Form 1120 address instead of the Ogden PIN Unit.

Forgetting to attach Form 5472, which is the whole point of the filing.

Leaving off the Foreign-owned U.S. DE notation across the top of the form.

Assuming no U.S. income means nothing to file, when funding the LLC already triggers it.

Frequently asked questions

Does an LLC file Form 1120?

It depends on how the LLC is taxed. An LLC that elects to be taxed as a corporation on Form 8832 files the real Form 1120. A foreign-owned single-member LLC left as a disregarded entity files only the near-empty pro forma Form 1120 with Form 5472. A US-owned single-member LLC that stays disregarded files neither, and its owner reports the activity instead. A multi-member LLC defaults to Form 1065, not Form 1120.

Is Form 1120 the same as Form 1120-S?

No. Form 1120-S is the U.S. Income Tax Return for an S corporation, a separate election that is generally not available to a nonresident-alien owner. Your disregarded LLC files neither one by default.

What about Form 1120-F?

Form 1120-F is the income tax return of a foreign corporation with U.S. income, not a disregarded LLC. If you worry that you count as a foreign corporation, see our guide to Form 1120-F and when it applies.

Do I owe U.S. corporate tax on the pro forma 1120?

No. The pro forma Form 1120 is an information return, not a tax computation. A disregarded entity owes no corporate income tax on it.

My LLC had no income. Do I still file?

Usually yes. If you had any reportable transaction, such as funding the company or taking a distribution, the filing is required even in a no-income year.

Get the current IRS forms

Always pull the latest revision straight from the IRS, since line numbers and instructions change year to year. A foreign-owned disregarded LLC uses these to assemble the pro forma package, not to complete a full corporate return.

How this article was prepared

The definition of Form 1120 and the rule that domestic corporations file it come from the IRS About Form 1120 page and the Instructions for Form 1120. The disregarded-entity default comes from the IRS single-member LLC guidance, and the double-tax description from the IRS Forming a Corporation page. The pro forma Form 1120, the section 6038A treatment, the filing channel, the deadline, and the 25,000 dollar penalty come from the Instructions for Form 5472. The continuation penalty and the no stated maximum are confirmed on the IRS international information reporting penalties page. The EIN and SS-4 wording come from the Instructions for Form SS-4. Last reviewed July 2026. For this review we confirmed the Ogden PIN Unit address, the 855-887-7737 fax channel, and the 25,000 dollar penalty against the current Instructions for Form 5472. The calendar-year deadline was checked against the Instructions for Form 1120. This is general information, not legal or tax advice, and CORPBOLT is a formation service, not a law or accounting firm. Treat all IRS dates, fax numbers, and addresses as the agency's current figures, and verify them on the live IRS pages before you file.

A quick note on CORPBOLT: CORPBOLT forms and maintains Wyoming LLCs for non-residents from $349/year (Foundation), including the registered agent and US business address. The EIN your pro forma filing depends on is included from $599/year (Launch) or as a $199 add-on, prepared for you on paper. We are a formation service, not a law firm or CPA, so talk to a qualified tax professional about your own filing. Start your US LLC.